2016 Theme #5: The Systemic Failure of High Finance

This week I am addressing themes I see playing out in 2016.

A number of systemic, structural forces are intersecting in 2016. One is the failure of high finance to fix the global economy's systemic problems.

The operative conceit of the past 7 years has been that high finance can fix whatever's broken in the world's economies. According to this narrative, all the world needed to boost "growth," employment and profits was lower interest rates, more liquidity, reverse repos and some other fancy financial footwork.

Once all this high finance generated more borrowing by debt-serfs, property developers, students, corporations buying back their shares and financiers skimming billions from asset bubbles, systemic problems would be dissolved or mitigated.

Cheap credit, asset bubbles and immense profiteering by financiers would heal all wounds and make everything better for everyone, even those at the bottom layer of the economy.

Unfortunately, this isn't true. High finance and cheap credit have intensified structural problems such as rising inequality, not resolved them.

The implicit promise of the neoliberal project is that liberalizing private-sector markets and credit will magically grease the processes of growth and widespread prosperity.

When economies have the right systems in place--decentralized, somewhat free markets, an entrepreneurial spirit, many unmet needs, idle productive capacity and a credit-starved real economy--freeing up static markets and credit can unleash the productive capacity of the bottom level of the economy.

But in economies dominated by state/private monopolies and cartels, neoliberalism simply funnels the profits of financialization to the few at the expense of the many, and at the cost of heightened instability and insecurity.

Making more credit available for student loans didn't fix America's broken higher education system--it only tightened the grip of the higher education cartel and turned another generation of students into debt-serfs.

Loosening mortgage standards and lowering interest rates didn't turn America into an "ownership society"--it turned it into a boom-and-bust speculative society with many more losers than winners in the neoliberal/high finance speculative casino.

The essence of neoliberal high finance is the vast majority of gamers in the casino lose security and wealth, while the House (the state and the banks) skim the resulting profits. Main Street has found its security stripped away (sorry, Bucko, no yield on savings now; you have to belly up and place a high-risk bet at a gaming table to keep what you had before) in exchange for the potential of outsized profits.

But alas, the games are rigged; the financiers have first access to the Federal Reserve's nearly free money, and insiders profit from stock buybacks and other financial gaming that generates monumental profits but zero goods and services.

If debt had grown in parallel with GDP and inflation, total credit market debt in the U.S. would be around $20+ trillion rather than $59 trillion. The difference is speculative excess, manifested in asset bubbles and staggering amounts of debt.

The casino's losers get the debt, the winners skim the profits.

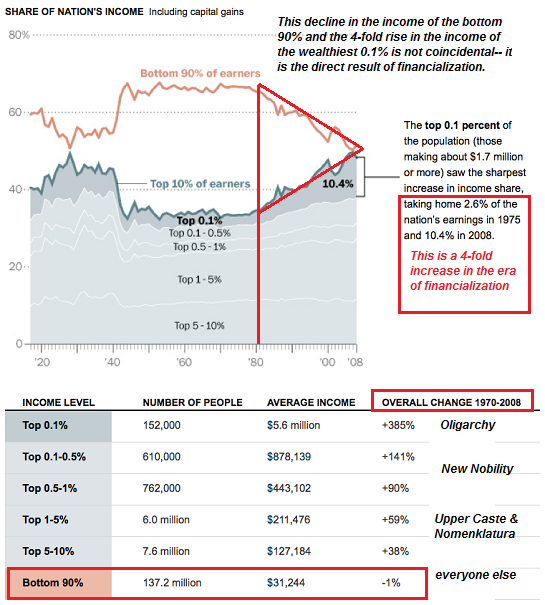

The only possible output of this system is rising income and wealth inequality:

Cheap credit doesn't reverse the elimination of jobs via automation--it accelerates that process by making capital machinery and software cheaper than labor and labor overhead.

Cheap credit and high finance don't fix what's broken in our democracy--they have greased the skids to what we have now--"democracy" for the highest bidder by giving financiers and corporations the means to stripmine productive assets and use the gargantuan profits to buy political favors.

High finance isn't the cure--it's the disease.

My book on the emerging economy is now available as a audiobook: Get a Job, Build a Real Career and Defy a Bewildering Economy (Audible.com).

My new book is #7 in Amazon's Kindle ebooks > Business & Money > International Economics: A Radically Beneficial World: Automation, Technology and Creating Jobs for All. The Kindle edition is $$9.95 and the print edition is currently discounted to $21.60.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, David K. ($200), for yet another outrageously generous contribution to this site -- I am greatly honored by your steadfast support and readership.

|

Thank you, Ron R. ($60), for yet another astoundingly generous contribution to this site -- I am greatly honored by your steadfast support and readership.

|